Freedom Capital Management September Market Update (Click for full article)

September 11, 2021

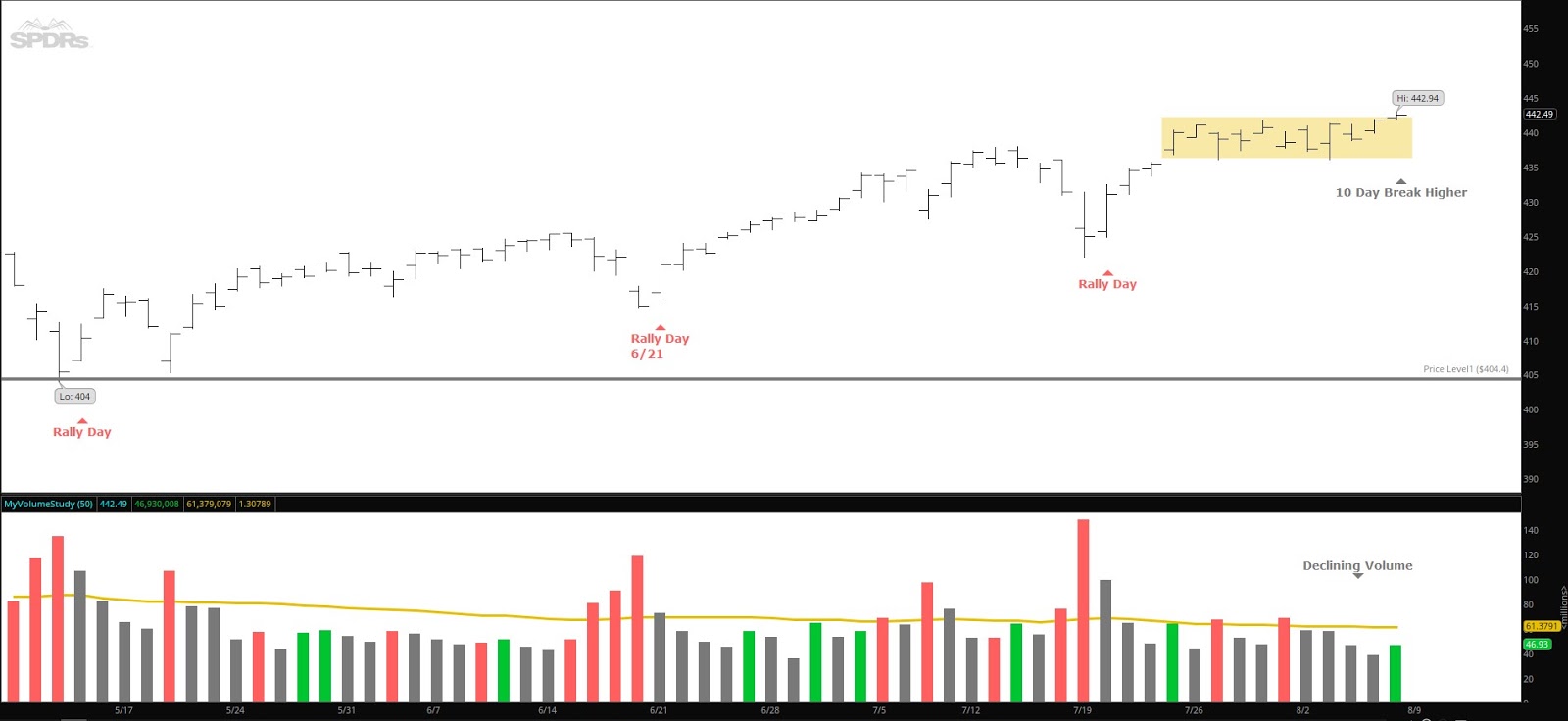

As a portfolio manager I try to keep my emotions out of our trading. I rely on market indicators to signify the strength of the markets. I have mentioned in past newsletters how certain months in the market historically underperform. Well, two of the months July and August, are over. The surge with the Corona Virus is concerning but hasn’t affected the Markets. My concern now is that the indicators that I rely on for market strength are indicating declining market strength. Nothing that is alarming, but it is noticeable. First to notice is the decline in trading volume, but reduced volume is normal during summer months. Also, there are less stocks trading above their 200-day moving average than last month. Last month’s reading was 83% this month is 73%. This indicator has been declining since April. The Advance/Decline line is weakening. And the VIX Index has been rising since June 29th. Markets don’t go up forever, they just seem to be slowing down, for now. The markets are still trading near the all-time highs!

Below is a Year to Date (YTD) chart of the Nasdaq 100 ETF, “QQQ.”

Markets can turn on a dime quickly, for now I remain encouraged by the overall upward direction.

The VIX Index closed at 20.95 on Friday 9/10. The VIX is rising and while the market trades lower. A falling VIX is bullish for the markets. I prefer the VIX below 20 and a VIX below 15 is even more bullish.

Percent of stocks above their 50 day and 200 day moving average: Last month 62% of stocks were above their 50-day moving average, this month 50% are above their 50-day moving average. Last month 83% of the stocks are above their 200-day moving average, today 73% are above their 200-day moving average. When 60% of stocks are above their 200-day moving average and the 50-day is rising, that is bullish. It would be a sign of strength if the stocks above their 50-day moving average begin to rise higher.

Federal Reserve: The next FOMC meeting announcement will be September 22nd. A comment from the FOMC press release from July 28th: “The path of the economy continues to depend on the course of the virus. Progress on vaccinations will likely continue to reduce the effects of the public health crisis on the economy but risks to the economic outlook remain”.

Unemployment Rate: Total nonfarm payroll employment rose by 235,000 in August, and the unemployment rate declined by 0.2 percentage point to 5.2 percent, the U.S. Bureau of Labor Statistics reported on Sept 3, 2021. So far this year, monthly job growth has averaged 586,000. In August, notable job gains occurred in professional and business services, transportation and warehousing, private education, manufacturing, and other services. Employment in retail trade declined over the month.t

Inflation Rate: The annual inflation rate for the United States is 5.3% for the 12 months ended August 2021, following two straight 5.4% increases, according to U.S. Labor Department data published September 14. The next inflation update is scheduled for release on October 13 at 8:30 a.m. ET. It will offer the rate of inflation over the 12 months ended September 2021.

The 10-year Treasury index yield: Is at 1.27%, not much change from last month at 1.29%.

Overall, the markets have an upward bias, trading near new highs recently, and continue to show strength, buy trading is choppy with an increasing VIX index rating. I would suggest caution at this time.

NOTE: To view past Market Newsletters, go to www.freedomcapitalmanagement.com and on the home page you will see recent newsletters and for older newsletters go to the blog page tab at the top of the home page.

In this month’s recap: Stocks rallied, fueled by an improving labor market, strong corporate earnings, and clarity on Fed tapering plans.

Monthly Economic Update

![]()

Presented by Guy Woolley, September 2021

U.S. Markets

Signs of an improving labor market, strong corporate earnings, and more clarity from the Fed on its tapering plans propelled stocks to multiple record highs during August.

The Dow Jones Industrial Average gained 1.22 percent while the Standard & Poor’s 500 Index rose 2.90 percent. The Nasdaq Composite led, picking up 4.00 percent.1

Corporate Earnings

Corporate profits in the second quarter were by all measures exceptional. With 98 percent of companies in the S&P 500 index reporting, 89 percent beat Wall Street consensus estimates by an average of 17.7 percent. The companies posted an earnings-per-share growth of nearly 92 percent over the second quarter of 2020.2

The labor market also showed signs of improving health, providing evidence that the economic recovery remained intact. In August, jobless claims reached pandemic lows, while employers added 953,000 jobs in July, and job openings reached record levels.3

Fed at Center Stage

In the final days of trading, Fed Chair Jerome Powell stated that the Fed might begin to pare back its monthly bond purchases before year-end. Powell’s update followed multiple comments from regional Federal Reserve Bank presidents indicating their support for reducing bond purchasing. It’s important to note that Powell said that tapering should not be seen as an indicator of future changes in interest rates.4

COVID Worries

The month was not without its worries. The global spread of the Delta variant resulted in flashes of investor anxiety that led to temporary pullbacks in stock prices. New COVID-19 cases in the U.S. rose throughout August, raising concerns that spreading infections could derail the economic recovery.5

In Asia, outbreaks closed some shipping ports. Vietnam partially halted manufacturing, and Japan extended its lockdown protocols. These actions raised concerns about their supply chain impact and what it may mean for inflation and economic growth.

Sector Scorecard

For the second straight month, energy was the only industry sector under pressure. Energy lost 1.34 percent in August. Otherwise, gains were posted in Communication Services (+3.52 percent), Consumer Discretionary (+1.54 percent), Consumer Staples (+0.83 percent), Financials (+5.28 percent), Health Care (+2.45 percent), Industrials (+1.39 percent), Materials (+2.19 percent), Real Estate (+2.20 percent), Technology (+4.1 percent), and Utilities (+4.02 percent).6

What Investors May Be Talking About in September

Since the early days of the pandemic, Fed Chair Jerome Powell has maintained that accommodative monetary policies would remain unchanged until the economy recovered. He’s been clear that the Fed would be very transparent in communicating monetary policy changes well ahead of implementing them to allow the capital markets sufficient time to digest any change.

Comments by a number of Federal Reserve Bank regional presidents last month may have heralded the beginning of a communication plan.

First, the Federal Reserve Banks of Atlanta and Richmond made comments, suggesting that the time to begin tapering was nearing. This was followed days later by remarks from the Federal Reserve Banks of Dallas and Kansas City, indicating that the economy had progressed enough to commence tapering as early as October.7,8

Talk of tapering grew louder with the August 18th release of the FOMC (Federal Open Market Committee) meeting minutes, suggesting that the Fed may be ready to scale back its bond purchases before year-end.

Finally, a speech by Fed Chair Jerome Powell near the end of the month confirmed that the Fed was getting closer to the start of tapering. Powell indicated that tapering could begin before year-end in his prepared comments, though he cautioned against connecting tapering with an interest rate hike.9

For many market observers, the Fed appears to be signaling that its September meeting may lead to changes in language and policy. The two-day meeting ends on September 22nd.

![]()

T I P O F T H E M O N T H

![]()

If you’re shopping for a homeowner policy, feel free to ask for a discount. If you can demonstrate that you are taking steps to manage risk, you may be able to negotiate one.

![]()

World Markets

A strong U.S. equity market helped push international stocks higher, with the MSCI-EAFE Index advancing 1.60 percent in August.10

In Europe, Germany tacked on 1.87 percent, the U.K. added 1.24 percent France picked up 1.02 percent.11

The Pacific Rim markets were mixed. Japan rose 2.95 percent and Australia rose 1.92 percent. But China’s Hang Seng index and Korea’s KOSPI edged lower.12

Indicators

Gross Domestic Product: The pace of economic growth in the second quarter was revised upward slightly, from 6.5 percent to 6.6 percent annualized rate.13

Employment: Employers added 943,000 new jobs in July—the biggest jump since August 2020. The unemployment rate fell to 5.4 percent, down from June’s 5.9 percent rate.14

Retail Sales: Retail sales cooled in July, falling 1.1 percent, led by a decline in auto purchases. Retailers attributed the weakness to the spread of the Delta variant.15

Industrial Production: Output at the nation’s factories, mines, and utilities rose 0.9 percent, led by a 1.4 percent rise in manufacturing production. July’s result topped the consensus estimate of a 0.5 percent increase.16

Housing: Housing starts slid 7.0 percent as challenges with land, labor, and materials persisted.17

Existing home sales rose 2.0 percent as limited inventory and strong demand drove the median price higher by nearly 18 percent to $359,900 from July 2020.18

For the first time in four months, new home sales rose, increasing 1.0 percent as the median sales price jumped 18.4 percent to a record level of $390,500.19

Consumer Price Index: Consumer prices climbed at their fastest rate since 2008, rising 0.5 percent in July and by 5.4 percent year-over-year.20

Durable Goods Orders: New orders of goods designed to last three years or more declined 0.1 percent in July, dragged down by a nearly 50 percent drop in nondefense aircraft and parts.21

![]()

Q U O T E O F T H E M O N T H

“Perform at your best when your best is required. Your best is required each day.”

JOHN WOODEN

![]()

The Fed

Minutes from the July 27-28 FOMC meeting revealed that some appeared ready to slow the pace of monthly bond purchases by the end of the year.22

“Various participants commented that economic and financial conditions would likely warrant a reduction in coming months,” according to the minutes.

“Several others indicated, however, that a reduction in the pace of asset purchases was more likely to become appropriate early next year because they saw prevailing conditions in the labor market as not being close to meeting the Committee’s ‘substantial further progress’ standard or because of uncertainty about the degree of progress toward the price-stability goal.”23

|

MARKET INDEX |

Y-T-D CHANGE |

August 2021 |

|

DJIA |

15.53% |

1.22% |

|

NASDAQ |

18.40% |

4.00% |

|

S&P 500 |

20.41% |

2.90% |

|

BOND YIELD |

Y-T-D |

August 2021 |

|

10 YR TREASURY |

0.38% |

1.30% |

Sources: Yahoo Finance, August 31, 2021.

The market indexes discussed are unmanaged and generally considered representative of their respective markets. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results. U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid.

![]()

T H E M O N T H L Y R I D D L E

![]()

What do the words Potato, Voodoo, Grammar, Revive and Banana have in common?

LAST MONTH’S RIDDLE: An auto dealership sold 150 cars in a special 6-day tent sale offer. Each day the dealership sold 6 more cars than the day before. How many cars were sold on the 6th day?

ANSWER: 40 cars. On the first day, the company sold x cars. On the second day, x + 6, on the third day, x + 12, on the fourth day, x + 18, on the fifth day, x + 24, and on the sixth day, x + 30. If you add all the days together you get the equation: x + (x + 6) + (x + 12) + (x + 18) + (x + 24) + (x + 30) = 150 cars sold. 6x + 90 = 150 and so x = 10. So, on day 6 (x + 30) = 40.

![]()

Guy Woolley may be reached at 415-236-5364 or [email protected]

www.freedomcapitalmanagement.com

Know someone who could use information like this?

Please feel free to send us their contact information via phone or email. (Don’t worry – we’ll request their permission before adding them to our mailing list.)

![]()

«RepresentativeEmailDisclosure»

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs, or expenses. Investors cannot invest directly in indices. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalization in the FTSE Developed Europe Index. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. Established in January 1980, the All Ordinaries is the oldest index of shares in Australia. It is made up of the share prices for 500 of the largest companies listed on the Australian Securities Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The FTSE TWSE Taiwan 50 Index is a capitalization-weighted index of stocks comprising 50 companies listed on the Taiwan Stock Exchange developed by Taiwan Stock Exchange in collaboration with FTSE. The MSCI World Index is a free-float weighted equity index that includes developed world markets and does not include emerging markets. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The U.S. Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability, and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting, or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

CITATIONS:

1. WSJ.com, August 31, 2021

2. Twitter.com/EarningsScout, August 26, 2021. 490 companies S&P 500 companies reported through August 26.

3. WSJ.com, August 26, 2021

4. WSJ.com, August 27, 2021

5. CDC.gov, August 27, 2021

6. Sectorspdr.com, August 31, 2021

7. Reuters.com, August 9, 2021

8. WSJ.com, August 11, 2021

9. WSJ.com, August 27, 2021

10. MSCI.com, August 31, 2021

11. MSCI.com, August 31, 2021

12. MSCI.com, August 31, 2021

13. CNBC.com, August 26, 2021

14. WSJ.com, August 6, 2021

15. WSJ.com, August 17, 2021

16. MarketWatch.com, August 17, 2021

17. Bloomberg.com, August 18, 2021

18. WSJ.com, August 23, 2021

19. Bloomberg.com, August 24, 2021

20. WSJ.com, August 11, 2021

21. WSJ.com, August 25, 2021

22. WSJ.com, August 18, 2021

23. FederalReserve.gov, July 28, 2021