Freedom Capital Management December Market Update (Click for Full Article)

December 13, 2021

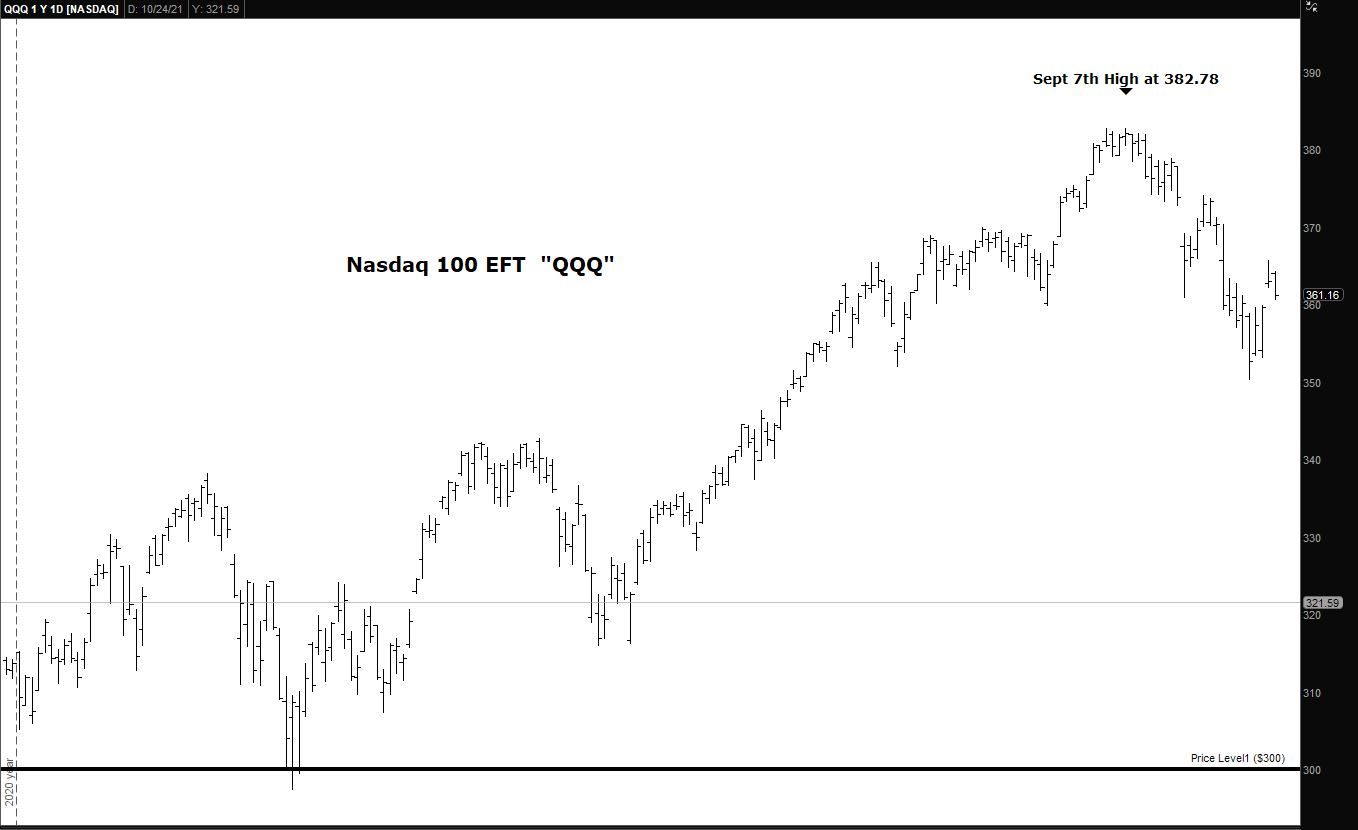

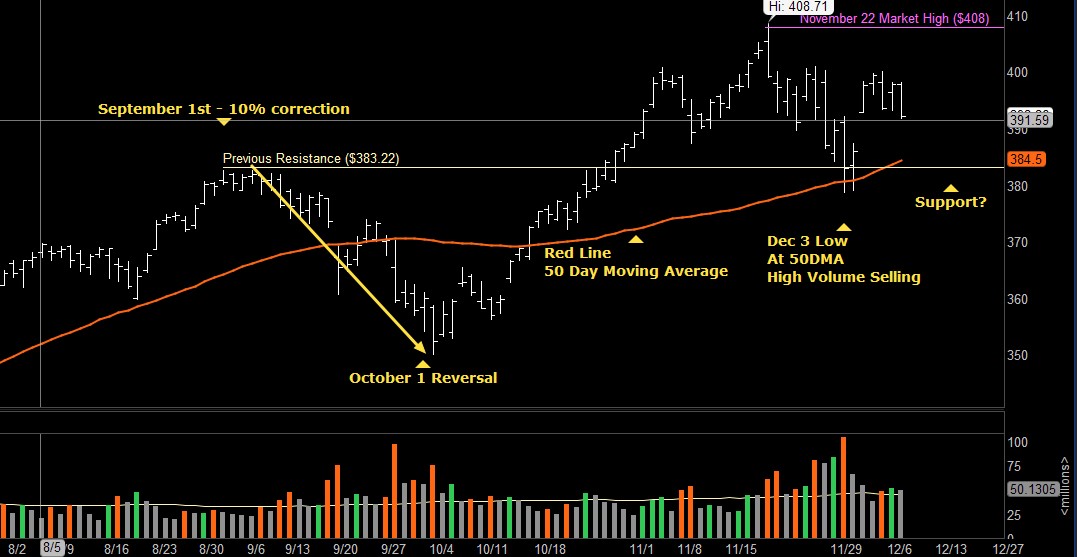

The chart above is of the Nasdaq 100 Exchange Traded Fund, Symbol “QQQ” from August 1st to today December 13th. After the 10% correction in the month of September the market has rallied back but without much progress higher. Also notice the up and down “choppy” action since November 1st. News events such as the coronavirus Omicron variant, imposed international travel restrictions, and the concerns over inflation have shaken the markets. The red line on the chart is the 50 Day moving average. Traders become defensive when the markets break their 50 averages. On December 3rd we broke that line on high volume but rallied above it the very next day. Also note that previous market resistance from September 1st is exactly where the 50 DMA is today. Many times, the previous resistance becomes the market support area. I expect the market volume to decline for the next two weeks due to reduced Holiday trading, although this week we have a FOMC meeting that always seems to rock the markets for a few days even when there is no change in the Federal Reserve rate. In fact, according to the FedWatch tool on the CME website there is a 95% chance that the FOMC will not raise rates until next year. I’d like to take a moment to wish everyone a wonderful holiday season and a very Happy and Healthy New Year!

The VIX Index closed at 27.19 last month, today it closed at 20.31. A falling VIX is normally bullish for the markets. I prefer the VIX below 20 and a VIX below 15 is even more bullish.

Percent of stocks above their 50 day and 200 day moving average: Last month 66% of stocks were above their 50-day moving average, this month 55% are above their 50-day moving average. Last month 72% of the stocks are above their 200-day moving average, today 67% are above their 200-day moving average. When 60% of stocks are above their 200-day moving average and the 50-day is rising, that is bullish. It would be a sign of strength if the stocks above their 50-day moving average begin to rise higher.

Federal Reserve: The next FOMC meeting announcement will be Wednesday December 15th. Expectations are that the Federal Reserve will not raise rates until March or May in 2022.

Unemployment Rate: Total nonfarm payroll employment rose by 210,000 in November, and the unemployment rate fell by 0.4 percentage point to 4.2 percent, the U.S. Bureau of Labor Statistics reported on December 3rd. Notable job gains occurred in professional and business services, transportation and warehousing, construction, and manufacturing. Employment in retail trade declined over the month.

Inflation Rate: The annual inflation rate for the United States is 6.8% for the 12 months ended November 2021 — the highest since June 1982 and after rising 6.2% previously, according to U.S. Labor Department data published December 10. The next inflation update is scheduled for release on January 12, 2022, at 8:30 a.m. ET. It will offer the rate of inflation over the 12 months ended December 2021.

The 10-year Treasury index yield: The rate on today is was at 1.42%, Lower than last months close at 1.55%

Trading continues to be choppy. If you have considered refinancing your home I would suggest you look into this while mortgage interest rates are still historically low.

To view past Market Newsletters, go to www.freedomcapitalmanagement.com and on the home page you will see recent newsletters and for older newsletters go to the blog page tab at the top of the home page.

In this month’s recap: Reports of a new COVID-19 variant blindsided markets as a wave of late selling erased the month’s earlier gains.

Monthly Economic Update

![]()

Presented by Guy Woolley, December 2021

U.S. Markets

Reports of a new COVID-19 variant in late November roiled markets as a wave of selling erased the month’s earlier gains.

The Dow Jones Industrial Average took the hardest hit, dropping 3.73 percent. The Standard & Poor’s 500 Index fell 0.83 percent while the Nasdaq Composite managed a small gain of 0.25 percent.1

Thanksgiving Surprise

The markets were blindsided by news over Thanksgiving Day of the emergence of a new strain of COVID-19, which led to travel bans by multiple countries and renewed unease about the prospect of a return to economic and social restrictions.

The potential global spread of this new COVID-19 variant Omicron triggered fears of another round of economic deceleration, sending investors back to their pandemic playbook of selling travel and leisure, financials, energy, and cyclicals and buying pharmaceutical companies and stay-at-home stocks.

Volatile Trading

The sharp drop on Friday, November 26, was exacerbated by reduced liquidity in the markets due to many traders being absent on this normally quiet post-holiday, shortened trading session. Stocks rebounded as traders returned to work on the following Monday but were unable to hold their gains on the month’s final trading day.

Upbeat Company Reports

The month had started off on a strong note, helped by a string of positive corporate earnings surprises, optimistic forward guidance from companies, and solid economic data. Investors were particularly encouraged by the fact that businesses had navigated the challenges of a surge in Delta variant infections in the third quarter, rising inflation, and supply chain bottlenecks.

Fed Headlines

Developments in Federal Reserve policy dominated much investor attention throughout the course of November. The first of these was the Fed announcement that it would begin its bond tapering program. Markets were unfazed by this news as they had long anticipated that the Fed would soon commence paring back its monthly bond purchases.

The second was the uncertainty surrounding whether Jerome Powell would be renominated to serve another four years as Fed chair. When President Biden finally announced his decision to renominate Powell, bond yields rose as investors became more certain that the Fed’s monetary normalization policy would proceed as planned.

Omicron Uncertainty

The consensus narrative of healthy economic expansion in 2022 was left a bit dented by the introduction of the Omicron variant. Many questions surround the new variant and its impact on global economies. Markets don’t always respond efficiently within an information void, creating the potential for further volatility until more is known about Omicron.

Sector Scorecard

Industry sector performance was mixed in November. Gains were posted in Consumer Discretionary (+3.03 percent), Consumer Staples (+1.25 percent), Materials (+1.97 percent), Real Estate (+1.21 percent), Technology (+5.33 percent), and Utilities (+1.26 percent). Losses were experienced in Communications Services (-3.06 percent), Energy (-2.73 percent), Financials (-3.40 percent), Health Care (-1.11 percent), and Industrials (-1.05 percent).2

What Investors May Be Talking About in December

In the coming weeks, markets will be sorting out news from Washington, updates on COVID variant Omicron, and economic reports.

On the economic front, investors are expected to keep a close eye on retail sales for the month of November, which are scheduled for release December 15. The November report will include the post-Thanksgiving start to the holiday shopping season and potentially be an advanced read on whether the supply chain bottlenecks might hamper holiday sales.3

Another anticipated report will be the Consumer Price Index, which will give an update on inflation trends. It’s due on December 10. If inflation continues to run hot, it may test investor confidence.4

![]()

T I P O F T H E M O N T H

![]()

Exercise is not only wise, it may also prove economical. In the long run, just keeping fit may save you thousands of dollars (or more) in medical bills that an unhealthy person may incur.

![]()

World Markets

A resurgence of Delta variant infections, spreading economic and social restrictions, and the emergence of a new COVID-19 variant sent international stocks broadly lower, with the MSCI-EAFE Index falling 3.79 percent in November.5

Major European markets dropped, with losses in Germany (-3.75 percent), the U.K. (-2.46 percent), and France (-1.60 percent).6

Pacific Rim markets also were under pressure. Hong Kong lost 7.49 percent, Japan tumbled 3.71 percent, and Australia slipped 0.92 percent.7

Indicators

Gross Domestic Product: Economic growth in the third quarter was revised slightly higher, to 2.1 percent from 2.0 percent.8

Employment: Job growth rebounded as employers added 531,000 jobs in October. The unemployment rate fell to 4.6 percent, though the labor participation rate stayed stubbornly low at 61.6 percent.9

Retail Sales: Retail sales rose 1.7 percent, exceeding expectations. This gain was, in part, attributed to higher costs and the pulling forward of holiday shopping as consumers worried about low inventory during the holiday season.10

Industrial Production: Industrial output rose 1.6 percent in October, reversing September’s slide. About half of the monthly gain was attributed to the recovery from Hurricane Ida.11

Housing: Housing starts slipped 0.7 percent in October, a surprise downturn for market watchers who had expected an increase.12

Existing home sales rose 0.8 percent, though it was off 5.8 percent from October 2020, which represents a cyclical high.13

New home sales increased 0.4 percent, though they were lower by 23.0 percent from a year earlier. The median price jumped nearly 18.0 percent year-over-year to $407,700.14

Consumer Price Index: The prices of consumer goods and services increased 0.9 percent in October and jumped by 6.2 percent year-over-year. This represented the fifth straight month of over 5 percent annualized inflation and the sharpest year-over-year increase since 1990.15

Durable Goods Orders: Orders for long-lasting goods fell 0.5 percent, the second straight month of declines. However, excluding transportation, durable goods orders increased by 0.5 percent.16

![]()

Q U O T E O F T H E M O N T H

“Create the highest, grandest vision possible for your life, because you become what you believe.”

OPRAH WINFREY

![]()

The Fed

Minutes from the November Federal Open Market Committee (FOMC) meeting showed an increasing concern over the persistence of inflation with the admission that inflationary pressures may take longer to abate than previously anticipated.

“The (Fed’s) near-term outlook for inflation was revised up, as consumer food and energy prices had risen faster than expected and production bottlenecks and recent wage gains were seen as putting somewhat greater upward pressure on prices than had been anticipated,” according to the minutes released following the Fed’s two-day meeting that ended November 3.17

Reflecting that concern, several officials suggested that the Fed’s bond tapering program may have to be accelerated in order to be ready to raise rates should inflation persist.18

| MARKET INDEX | Y-T-D CHANGE | November 2021 |

| DJIA | 12.67% | -3.73% |

| NASDAQ | 20.56% | 0.25% |

| S&P 500 | 21.59% | -0.83% |

| BOND YIELD | Y-T-D | November 2021 |

| 10 YR TREASURY | 0.52% | 1.44% |

Sources: Yahoo Finance, November 30, 2021

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year Treasury real yield = projected return on investment, expressed as a percentage, on the U.S. government’s 10-year bond.

![]()

T H E M O N T H L Y R I D D L E

![]()

You see a large truck stopped just before the underpass of a low bridge. The driver informs you that his truck is 1″ higher than the maximum clearance. This is the only road to his destination. What is the easiest way to help him get his truck through the underpass?

LAST MONTH’S RIDDLE: When can you add two to eleven and get one as the correct answer?

ANSWER: When you are figuring time. When you add two hours to eleven o’clock, you get one o’clock.

![]()

Guy Woolley may be reached at 415-236-5364 or [email protected]

www.freedomcapitalmanagement.com

Know someone who could use information like this?

Please feel free to send us their contact information via phone or email. (Don’t worry – we’ll request their permission before adding them to our mailing list.)

![]()

«RepresentativeEmailDisclosure»

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs, or expenses. Investors cannot invest directly in indices. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalization in the FTSE Developed Europe Index. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. Established in January 1980, the All Ordinaries is the oldest index of shares in Australia. It is made up of the share prices for 500 of the largest companies listed on the Australian Securities Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The FTSE TWSE Taiwan 50 Index is a capitalization-weighted index of stocks comprising 50 companies listed on the Taiwan Stock Exchange developed by Taiwan Stock Exchange in collaboration with FTSE. The MSCI World Index is a free-float weighted equity index that includes developed world markets and does not include emerging markets. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The U.S. Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability, and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting, or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

CITATIONS:

1. WSJ.com, November 30, 2021

2. SectorSpdr.com, November 30, 2021

3. Census.gov, 2021

4. BLS.gov, 2021

5. MSCI.com, November 30, 2021

6. MSCI.com, November 30, 2021

7. MSCI.com, November 30, 2021

8. CNBC. November 24, 2021

9. WSJ.com, November 5, 2021

10. CNBC.com, November 16, 2021

11. MarketWatch.com, November 16, 2021

12. CNBC.com, November 17, 2021

13. CNBC.com, November 22, 2021

14. APNews.com, November 24, 2021

15. WSJ.com, November 10, 2021

16. CNBC.com, November 24, 2021

17. FederalReserve.gov, November 24, 2021

18. WSJ.com, November 24, 2021

Guy Woolley

Registered Investment Advisor

Freedom Capital Management, Inc.

www.freedomcapitalmanagement.com

Direct: 415-236-5364

Toll Free: 866-357-2710

This email, including attachments, may include confidential and/or proprietary information, and may be used only by the person or entity to which it is addressed. If the reader of this email is not the intended recipient or his or her authorized agent, the reader is hereby notified that any dissemination, distribution or copying of this email is prohibited. If you have received this email in error, please notify the sender by replying to this message and delete this email immediately.

The information included herein was obtained from sources which we believe reliable, but we do not guarantee its accuracy. Neither the information nor any opinion expressed constitutes a solicitation by us for the purchase or sales of any securities or other financial instruments. The material is intended for the sole use of the person or firm to whom it is provided.