by Guy Woolley | Feb 11, 2022 | Finance

February 11, 2022

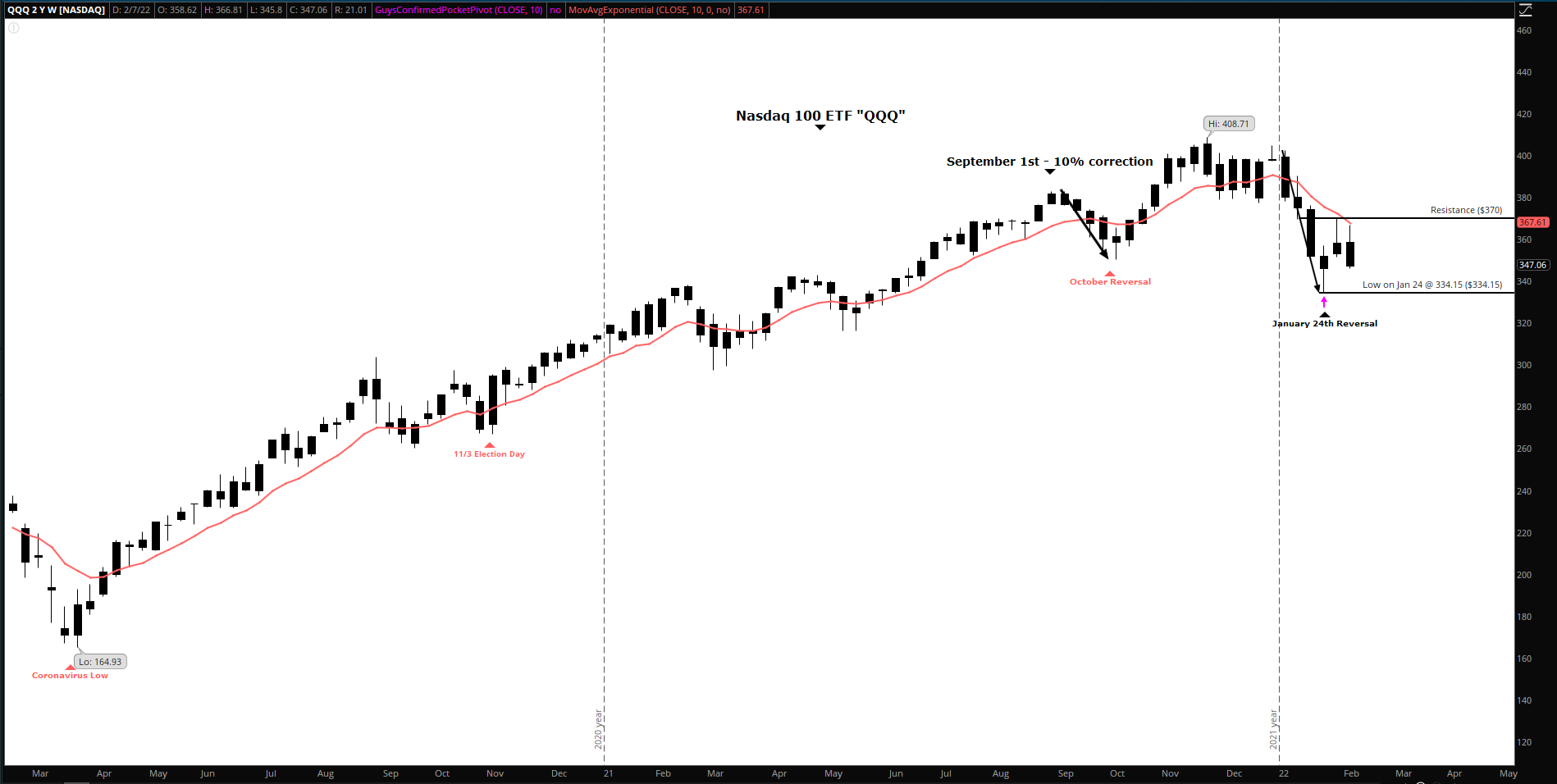

January was a “bearish” month for the market. The chart above is weekly chart of the Nasdaq 100 Exchange Traded Fund, Symbol “QQQ”. The vertical lines on the chart are year markings. The chart covers a time frame from March 2020 to Friday January 11th. The red line in the price chart is the 10-week exponential moving average, which the market respected for most of this period. We had a 10% correction in September 2021, which lasted a month before turning back up until the end of the year. The correction this past month has been sharper and deeper than September’s correction. Notice on the chart that the Nasdaq 100 is trading in the same price range as it was in September. We will be watching closely to see if the market will stay in this range. Regarding earnings reports, on Friday Factset reported “The index is reporting earnings growth of more than 30% for the fourth straight quarter and earnings growth of more than 45% for the full year. These above-average growth rates are due to a combination of higher earnings in 2021 and an easier comparison to weaker earnings in 2020 due to the negative impact of COVID-19 on a number of industries.” Right now, market volatility continues due to inflation, rising interest rates and the concern over the threat of a Russian invasion of Ukraine.

The VIX Index closed at 27.36 slightly higher than last month at 24.83. A rising VIX is normally bearish for the markets. I prefer the VIX below 20 and a VIX below 15 is more bullish.

Percent of stocks above their 50 day and 200 day moving average: Last month 59% of stocks were above their 50-day moving average, this month only 40% are above their 50-day moving average. Last month 69% of the stocks are above their 200-day moving average, today only 45% are above their 200-day moving average. When 60% of stocks are above their 200-day moving average and the 50-day is rising, that is bullish. A sign of strength would be if the stocks above their 50-day moving average begin to rise higher, and even stronger when the 50DMA is above the 200DMA.

Federal Reserve: The next FOMC meeting announcement will be Wednesday March 16th. There is a 98% expectation that the Federal Reserve will raise rates at least a quarter percent.

Unemployment Rate: Total nonfarm payroll employment rose by 467,000 in January, and the unemployment rate was little changed at 4.0 percent, the U.S. Bureau of Labor Statistics reported February 4th. Employment growth continued in leisure and hospitality, in professional and business services, in retail trade, and in transportation and warehousing.

Inflation Rate: The annual inflation rate for the United States is 7.5% for the 12 months ended January 2022 — the highest since February 1982 and after rising 7.0% previously, according to U.S. Labor Department data published February 10. The next inflation update is scheduled for release on March 10 at 8:30 a.m. ET. It will offer the rate of inflation over the 12 months ended February 2022.

The 10-year Treasury index yield: The rate today is at 1.93%, higher than last month’s close at 1.76%

Trading continues to be choppy. Again, if you have considered refinancing your home, I would suggest you investigate this while mortgage interest rates are still historically low.

To view past Market Newsletters, go to www.freedomcapitalmanagement.com and on the home page you will see recent newsletters and for older newsletters go to the blog page tab at the top of the home page.

In this month’s recap: Stocks fell as rising bond yields, elevated inflation, and a hawkish-sounding Fed took turns rattling investor confidence.

Monthly Economic Update

Presented by Guy Woolley, February 2022

U.S. Markets

Rising yields, elevated inflation, and a hawkish-sounding Fed took turns rattling the stock market in January, with technology-heavy Nasdaq particularly hard hit.

The Dow Jones Industrial Average dropped 3.32 percent, while the Standard & Poor’s 500 Index fell 5.26 percent. The Nasdaq lost 8.98 percent.1

Fear of the Fed

Anxiety about the Federal Reserve’s pivot from its accommodative monetary policy toward monetary normalization hung over the market all month.

Early in the month, the Fed released the minutes from its December meeting, which suggested a more hawkish tone than what investors were expecting.

Inside the Fed minutes, the first update that unsettled markets was the likelihood of an interest rate increase in March, which would be sooner than many had expected. The second update that upset investors was news that the Fed was considering reducing its balance sheet, a step toward tightening that had not been widely anticipated.

More from the Fed

Following its January meeting, Fed Chair Powell indicated that reducing the balance sheet might come at a faster pace than the balance sheet reductions in 2014 and 2018.

Bond yields trended higher in response to Powell’s news. Higher yields hurt technology and other high-valuation companies the most.

Economic Recovery

Amid the stock market turbulence, the underlying fundamentals showed a solid economic recovery. Unemployment fell, housing was strong, and fourth-quarter Gross Domestic Product rose beyond consensus expectations. But hot inflation tempered enthusiasm.

Earnings Underway

A strong start to the fourth quarter earnings season caught investor’s attention. Of the 33 percent of the companies comprising the S&P 500 Index that reported by month’s end, 77 percent reported earnings above Wall Street estimates. While the total “beat” percentage was higher than average, the amount by which earnings actually beat analysts’ estimates was by a narrower margin.2

Stocks rallied sharply in the final two sessions, taking the edge off an otherwise challenging month for investors.

Sector Scorecard

Except for Energy (+17.07 percent), all industry sectors closed the month with losses, including Communications Services (-8.27 percent), Consumer Discretionary (-13.23 percent), Consumer Staples (-1.05 percent), Financials (-1.33 percent), Health Care (-7.07 percent), Industrials (-5.54 percent), Materials (-7.70 percent), Real Estate (-8.48 percent), Technology (-10.09 percent), and Utilities (-3.86 percent).3

What Investors May Be Talking About in February

With the fourth quarter earnings season well underway, investors will continue to focus on earnings reports throughout the month. Expect investors to continue to focus on quarterly reports from high-valuation growth companies.

Earnings from such companies may have a high bar to clear with investors amid expectations for a continued climb in bond yields.

As investors saw in January, these high-multiple stocks can come under pressure as bond yields trend higher. The reason for this is twofold. First, when rates tick up, it’s more difficult to forecast future earnings. Second, higher rates may increase a firm’s cost of capital.

T I P O F T H E M O N T H

Students who want to enter college this fall should complete the FAFSA early in the year to increase eligibility for student aid. After completing it, they should apply for scholarships as soon as possible.

World Markets

Overseas markets fell in tandem with the U.S., as the MSCI-EAFE Index sank 5.76 percent in January.4

Major European markets were broadly lower, with losses in Germany (-2.60 percent) and France (-2.15 percent). The U.K. was the only major European exchange that saw a gain (+1.08 percent).5

Pacific Rim markets were mostly down as well. Australia lost 6.35 percent and Japan dropped 6.22 percent. Hong Kong bucked the trend, gaining 1.73 percent.6

Indicators

Gross Domestic Product: The rate of economic expansion in the fourth quarter exceeded economists’ expectations, rising 6.9 percent—triple the growth rate of the third quarter. While the headline number was strong, two concerns emerged: Much of the growth was due to inventory build-up, and the price index for personal consumption expenditures (an inflation measure) accelerated from the third quarter, climbing 6.5 percent.7

Employment: Hiring slowed in December, with employers adding just 199,000 jobs—well below consensus estimates. The unemployment rate dropped to 3.9 percent, while wage growth rose 4.7 percent from a year ago, signaling a tight labor market. The December jobs report reflects data prior to the start of the Omicron variant spread in late December.8

Retail Sales: Retail sales declined by 1.9 percent. The spread of Omicron and early consumer holiday buying in response to possible inventory shortages dampened spending in December.9

Industrial Production: Industrial production contracted 0.1 percent. This dip was attributed to a decline in auto production and a drop in utility output due to warmer weather.10

Housing: Housing starts rose by 1.9 percent in the final month of 2021, helped by the warmest December on record. This increase occurred despite rising lumber prices and higher mortgage rates.11

Existing home sales slipped 4.6 percent, hampered by a higher year-over-year median sales price (+15.8 percent) and tight inventory.12

New home sales surged by 11.9 percent. With new homes, higher mortgage rates did not discourage buyers.13

Consumer Price Index: Consumer prices rose 0.5 percent in December, with inflation climbing 7.0 percent from a year ago. This year-over-year increase was the highest since 1982.14

Durable Goods Orders: Durable goods orders declined 0.9 percent to their lowest level since April 2020, reflecting the impact of the Omicron surge.15

Q U O T E O F T H E M O N T H

“What lies behind us and what lies before us are tiny matters compared to what lies within us.”

Ralph WALDO EMERSON

The Fed

The Federal Open Market Committee (FOMC) at its January meeting left rates unchanged, though officials signaled that rates would likely be raised at its next meeting in March.

The Fed also approved one last round of bond purchases, bringing quantitative easing to an end by March.

The FOMC did not offer details on its plan to shrink the Fed’s balance sheet. But Fed Chair Powell indicated that shrinking the Fed’s asset holdings may occur at a faster rate than in past periods of balance sheet reductions.16

| MARKET INDEX |

Y-T-D CHANGE |

January 2022 |

| DJIA |

-3.32% |

-3.32% |

| NASDAQ |

-8.98% |

-8.98% |

| S&P 500 |

-5.26% |

-5.26% |

|

|

|

| BOND YIELD |

Y-T-D |

January 2022 |

| 10 YR TREASURY |

.27% |

1.78% |

Sources: Yahoo Finance, January 31, 2022.

The market indexes discussed are unmanaged and generally considered representative of their respective markets. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results. U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid.

T H E M O N T H L Y R I D D L E

Add missing vowels to these three trios of letters to get the six-letter names of three different countries: PNM, MXC, KWT.

LAST MONTH’S RIDDLE: The English language has a noun with three consecutive double letters in it. The word is 10 letters long, and it describes a job involving math. What is this word?

ANSWER: Bookkeeper.

Guy Woolley may be reached at 415-236-5364 or [email protected]

www.freedomcapitalmanagement.com

Know someone who could use information like this?

Please feel free to send us their contact information via phone or email. (Don’t worry – we’ll request their permission before adding them to our mailing list.)

«RepresentativeEmailDisclosure»

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs, or expenses. Investors cannot invest directly in indices. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalization in the FTSE Developed Europe Index. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. Established in January 1980, the All Ordinaries is the oldest index of shares in Australia. It is made up of the share prices for 500 of the largest companies listed on the Australian Securities Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The FTSE TWSE Taiwan 50 Index is a capitalization-weighted index of stocks comprising 50 companies listed on the Taiwan Stock Exchange developed by Taiwan Stock Exchange in collaboration with FTSE. The MSCI World Index is a free-float weighted equity index that includes developed world markets and does not include emerging markets. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The U.S. Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability, and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting, or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

CITATIONS:

1. WSJ.com, January 31, 2022

2. Insight.FactSet.com, January 28, 2022

3. SectorSpdr.com, January 31, 2022

4. MSCI.com, January 31, 2022

5. MSCI.com, January 31, 2022

6. MSCI.com, January 31, 2022

7. WSJ.com, January 27, 2022

8. WSJ.com, January 7, 2022

9. WSJ.com, January 14, 2022

10. MarketWatch.com, January 14, 2022

11. CNBC.com, January 19, 2022

12. CNBC.com, January 20, 2022

13. USNews.com, January 26, 2022

14. WSJ.com, January 12, 2022

15. CNBC.com, January 27, 2022

16. WSJ.com, January 26, 2022

by Guy Woolley | Jan 10, 2022 | Finance

January 10, 2022

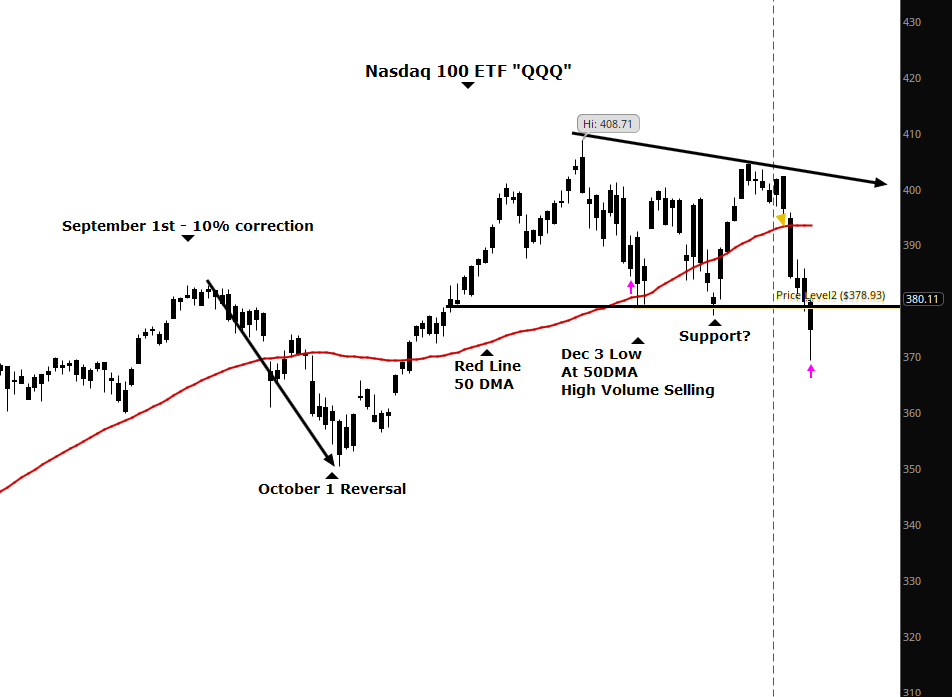

The chart above is of the Nasdaq 100 Exchange Traded Fund, Symbol “QQQ”. The vertical dotted line on the chart is the beginning of this new year 2022. (“Happy New Year!”) Last month’s newsletter I mentioned that it looked like the market would have support at the 380 level, which it found on December 20 then bounced up to a resistance level near 400. That move looked constructive and encouraging. Unfortunately, as the new year began interest rates spiked up and caused fear of the Federal Reserve’s pending rate hikes driving the market down. Today the market broke below the support area which only took 6 days from the beginning of the year! Today’s action is indicated with the small red arrow where the market broke support. But by the end of the day trading improved and returned up to the support area. This is a critical area to watch. I mentioned last month to clients that were thinking of refinancing their mortgages to take advantage of the low interest rates. I believe this quick action was a bit of an overreaction, which can happen in markets with trader’s being either too optimistic or too pessimistic. Looking back, I see that interest rates today are about where they were two years ago, before the corona virus pandemic. How quickly they are raised by the Federal Reserve this year we pay attention to. Corporate earning reports will be coming soon and many analysts are optimistic.

The VIX Index closed at 17.22 last month, today it closed at 19.40. A falling VIX is normally bullish for the markets. I prefer the VIX below 20 and a VIX below 15 is more bullish.

Percent of stocks above their 50 day and 200 day moving average: Last month 68% of stocks were above their 50-day moving average, this month 59% are above their 50-day moving average. Last month 72% of the stocks are above their 200-day moving average, today 69% are above their 200-day moving average. When 60% of stocks are above their 200-day moving average and the 50-day is rising, that is bullish. It would be a sign of strength if the stocks above their 50-day moving average begin to rise higher, and even stronger when the 50DMA is above the 200DMA.

Federal Reserve: The next FOMC meeting announcement will be Wednesday January 26th. There is only a 11% expectation that the Federal Reserve will raise rates a quarter percent.

Unemployment Rate: Total nonfarm payroll employment rose by 199,000 in December, and the unemployment rate declined to 3.9 percent, the U.S. Bureau of Labor Statistics reported On January 7th. Employment continued to trend up in leisure and hospitality, in professional and business services, in manufacturing, in construction, and in transportation and warehousing.

Inflation Rate: The annual inflation rate for the United States is 6.8% for the 12 months ended November 2021 — the highest since June 1982 and after rising 6.2% previously, according to U.S. Labor Department data published December 10. The next inflation update is scheduled for release on January 12, 2022, at 8:30 a.m. ET. It will offer the rate of inflation over the 12 months ended December 2021.

The 10-year Treasury index yield: The rate today is at 1.76%, higher than last month’s close at 1.42%

Trading continues to be choppy. Again, if you have considered refinancing your home I would suggest you look into this while mortgage interest rates are still historically low.

To view past Market Newsletters, go to www.freedomcapitalmanagement.com and on the home page you will see recent newsletters and for older newsletters go to the blog page tab at the top of the home page.

In this month’s recap: Stocks rally as early data suggests the health impact of Omicron was less severe than initially feared.

Monthly Economic Update

Presented by Guy Woolley, January 2022

U.S. Markets

Stocks rallied in December as early data suggested that the health impact of the Omicron variant was less severe than initially feared.

The Dow Jones Industrial Average picked up 5.38 percent, while the Standard & Poor’s 500 Index gained 4.36 percent. The Nasdaq Composite lagged, climbing 0.69 percent.1

Omicron Worries

Stocks got off to a volatile start in December as investors worried about Omicron’s transmissibility and severity. Markets were also rattled by Fed Chair Jerome Powell’s testimony to Congress that the economy was strong enough to allow the Fed to move up its bond purchase taper schedule.

While investors were expecting the Fed’s news, Powell’s testimony generated added uncertainty over just how sharp and rapid that pivot would be.

Fed Clarity

At its mid-December meeting, the Federal Open Market Committee said that it would quicken its tapering of monthly bond purchases from $15 billion a month to $30 billion a month. This acceleration in tapering meant that asset purchases by the Fed would likely end by March 2022.2

The Fed further signaled that it may consider up to three rate hikes, the first of which would likely occur sometime after bond tapering was completed.2

Santa Rally

With the year-end fast approaching and investor sentiment on Omicron’s economic impact becoming less fearful, investor attention turned to whether the market would enjoy a “Santa Claus Rally.”

The Santa Claus Rally is a seasonal pattern in which the market generally rises in the period following Christmas through the first two trading sessions of the new year. Since 1950, the S&P 500 has gained an average of 1.3 percent during this period and generated positive returns about 67 percent of the time since 1993.3

Cementing a Solid Year

This year, stocks rallied following the holiday but lost some momentum in the final two trading days. Nevertheless, stocks ended the year near all-time highs, cementing a solid year of gains for investors.

Sector Scorecard

All industry sectors posted positive performances last month with gains in Communications Services (+4.51 percent), Consumer Discretionary (+0.24 percent), Consumer Staples (+8.96 percent), Energy (+1.41 percent), Financials (+3.06 percent), Health Care (+9.06 percent), Industrials (+4.55 percent), Materials (+6.57 percent), Real Estate (+9.09 percent), Technology (+3.56 percent), and Utilities (+8.45 percent).4

What Investors May Be Talking About in January

In the month ahead, investors are expected to focus on fourth-quarter gross domestic product, scheduled for release on January 28.5

The Federal Reserve Bank of Atlanta, which models estimated GDP growth in real-time, said in late December it expects 7.6 percent growth. A strong GDP would confirm expectations of a rebound from the Delta variant-induced slowdown in the third quarter.5

Earnings Season

Fourth-quarter corporate earnings season will also kick off in January. According to FactSet, a financial data provider, consensus estimates are for a 20.9 percent growth in corporate earnings.6

The extent that earnings disappoint or exceed expectations may drive how markets view current stock price valuation levels.

T I P O F T H E M O N T H

If you’re financing a new car, look for the best interest rate before setting foot in the dealership. It could be to your advantage to take a cash rebate and get a loan elsewhere.

World Markets

Despite higher Omicron infections in Europe and isolated shutdowns in China, the MSCI-EAFE Index advanced 4.99 percent in December.7

Major European markets rebounded sharply from November losses, with gains in France (+6.43 percent), Germany (+5.20 percent), and the U.K. (+4.61 percent).8

Pacific Rim stocks had less impressive gains. Japan’s Nikkei index rose 3.49 percent while Australia’s ASX 200 gained 2.60 percent. China’s Hang Seng index lost 0.33 percent.9

Indicators

Gross Domestic Product: The final reading of GDP growth showed an upward revision to 2.3 percent from its prior estimate of 2.1 percent.10

Employment: The employment picture was mixed in November. Nonfarm jobs increased by a disappointing 210,000 but the unemployment rate fell to 4.2 percent as almost 600,000 Americans joined the workforce.11

Retail Sales: Retail purchases rose 0.3 percent, which was below expectations. The slight increase lends credence to the idea that October’s big jump was partly due to Americans buying early in response to possible inventory shortages.12

Industrial Production: Industrial production increased by 0.5 percent, reaching its highest level since January 2019. Manufacturing output was strong, rising 0.7 percent on a solid rebound in the auto sector.13

Housing: Housing starts increased 11.8 percent in November, which was above the consensus estimate of 3.0 percent.14

Existing home sales climbed 1.9 percent from October, though they slipped 2.0 percent from November 2020.15

New home sales rose 12.4 percent, reaching a seven-month high. Strong demand lifted the median sales price 18.8 percent from a year ago.16

Consumer Price Index: Consumer prices jumped at a rate not seen in nearly 40 years, rising 0.8% from the previous month and 6.8% from a year ago. It is the sixth consecutive month that inflation has exceeded 5%. Core inflation (excluding the more volatile food and energy prices) came in lower but still posted its sharpest jump since 1991.17

Durable Goods Orders: Orders of goods designed to last three years or more rose 2.5 percent, driven by a strong increase in commercial aircraft orders.18

Q U O T E O F T H E M O N T H

“It always seems impossible until it’s done.”

NELSON MANDELA

The Fed

After the two-day December meeting of the Federal Open Market Committee (FOMC), the Fed announced that it would be speeding up the pace of reductions in its monthly bond purchase, from the $15 billion per month announced in November to $30 billion per month, effectively ending asset purchases by March 2022. It also signaled that there may be as many as three increases in short-term interest rates in 2022.19

“In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook,” according to the Fed’s prepared statement.

“The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on public health, labor market conditions, inflation pressures and inflation expectations, and financial and international developments.”20

| MARKET INDEX |

Y-T-D CHANGE |

December 2021 |

| DJIA |

18.73% |

5.38% |

| NASDAQ |

21.39% |

0.69% |

| S&P 500 |

26.89% |

4.36% |

|

|

|

| BOND YIELD |

Y-T-D |

December 2021 |

| 10 YR TREASURY |

0.59% |

1.51% |

Sources: Yahoo Finance, December 31, 2021.

The market indexes discussed are unmanaged and generally considered representative of their respective markets. Individuals cannot directly invest in unmanaged indexes. Past performance does not guarantee future results. U.S. Treasury Notes are guaranteed by the federal government as to the timely payment of principal and interest. However, if you sell a Treasury Note prior to maturity, it may be worth more or less than the original price paid.

T H E M O N T H L Y R I D D L E

The English language has a noun with three consecutive double letters in it. The word is 10 letters long, and it describes a job involving math. What is this word?

LAST MONTH’S RIDDLE: You see a large truck stopped just before the underpass of a low bridge. The driver informs you that his truck is 1″ higher than the maximum clearance. This is the only road to his destination. What is the easiest way to help him get his truck through the underpass?

ANSWER: Let enough air out of the tires to lower the truck.

Guy Woolley may be reached at 415-236-5364 or [email protected]

www.freedomcapitalmanagement.com

Know someone who could use information like this?

Please feel free to send us their contact information via phone or email. (Don’t worry – we’ll request their permission before adding them to our mailing list.)

«RepresentativeEmailDisclosure»

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. The information herein has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. Investments will fluctuate and when redeemed may be worth more or less than when originally invested. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All market indices discussed are unmanaged and are not illustrative of any particular investment. Indices do not incur management fees, costs, or expenses. Investors cannot invest directly in indices. All economic and performance data is historical and not indicative of future results. The Dow Jones Industrial Average is a price-weighted index of 30 actively traded blue-chip stocks. The NASDAQ Composite Index is a market-weighted index of all over-the-counter common stocks traded on the National Association of Securities Dealers Automated Quotation System. The Standard & Poor’s 500 (S&P 500) is a market-cap weighted index composed of the common stocks of 500 leading companies in leading industries of the U.S. economy. The Russell 2000 Index measures the performance of the small-cap segment of the U.S. equity universe. The CBOE Volatility Index® (VIX®) is a key measure of market expectations of near-term volatility conveyed by S&P 500 stock index option prices. NYSE Group, Inc. (NYSE:NYX) operates two securities exchanges: the New York Stock Exchange (the “NYSE”) and NYSE Arca (formerly known as the Archipelago Exchange, or ArcaEx®, and the Pacific Exchange). NYSE Group is a leading provider of securities listing, trading and market data products and services. The New York Mercantile Exchange, Inc. (NYMEX) is the world’s largest physical commodity futures exchange and the preeminent trading forum for energy and precious metals, with trading conducted through two divisions – the NYMEX Division, home to the energy, platinum, and palladium markets, and the COMEX Division, on which all other metals trade. The SSE Composite Index is an index of all stocks (A shares and B shares) that are traded at the Shanghai Stock Exchange. The CAC-40 Index is a narrow-based, modified capitalization-weighted index of 40 companies listed on the Paris Bourse. The FTSEurofirst 300 Index comprises the 300 largest companies ranked by market capitalization in the FTSE Developed Europe Index. The FTSE 100 Index is a share index of the 100 companies listed on the London Stock Exchange with the highest market capitalization. Established in January 1980, the All Ordinaries is the oldest index of shares in Australia. It is made up of the share prices for 500 of the largest companies listed on the Australian Securities Exchange. The S&P/TSX Composite Index is an index of the stock (equity) prices of the largest companies on the Toronto Stock Exchange (TSX) as measured by market capitalization. The Hang Seng Index is a free float-adjusted market capitalization-weighted stock market index that is the main indicator of the overall market performance in Hong Kong. The FTSE TWSE Taiwan 50 Index is a capitalization-weighted index of stocks comprising 50 companies listed on the Taiwan Stock Exchange developed by Taiwan Stock Exchange in collaboration with FTSE. The MSCI World Index is a free-float weighted equity index that includes developed world markets and does not include emerging markets. The Mexican Stock Exchange, commonly known as Mexican Bolsa, Mexbol, or BMV, is the only stock exchange in Mexico. The U.S. Dollar Index measures the performance of the U.S. dollar against a basket of six currencies. Additional risks are associated with international investing, such as currency fluctuations, political and economic instability, and differences in accounting standards. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. MarketingPro, Inc. is not affiliated with any person or firm that may be providing this information to you. The publisher is not engaged in rendering legal, accounting, or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional.

CITATIONS:

1. WSJ.com, December 31, 2021

2. WSJ.com, December 15, 2021

3. CMEGroup.com, December 26, 2020

4. SectorSpdr.com, December 31, 2021

5. AtlantaFed.org, December 23, 2021

6. FactSet.com, December 2, 2021

7. MSCI.com, December 30, 2021

8. MSCI.com, December 30, 2021

9. MSCI.com, December 30, 2021

10. MarketWatch.com, December 22, 2021

11. WSJ.com, December 3, 2021

12. WSJ.com, December 15, 2021

13. ABCNews.go.com, December 16, 2021

14. Nasdaq.com, December 16, 2021

15. CNBC.com, December 22, 2021

16. Money.USNews.com, December 23, 2021

17. WSJ.com, December 10, 2021

18. Bloomberg.com, December 23, 2021

19. WSJ.com, December 15, 2021

20. FederalReserve,gov, December 15, 2021