June 11, 2023

One would think economic news would slow down after getting past last week’s debt limit deal that cut borrowing by $1.5 trillion. But this week we will be hearing more important economic numbers beginning on Tuesday. This week’s reports may have an impact on the markets.

Tuesday 6/13:

Consumer Price Index (CPI) measures the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Wednesday 6/14

The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output.

The Federal Reserve Funds Rate decision on the interest rate at which depository institutions lend balances held at the Federal Reserve to other depository institutions overnight. (As of today Monday, 6-12, there is only a 21% chance that the Fed will be raising again according to the CME FedWatch Tool.

Thursday 6/15

Empire State Manufacturing Index which is a gauge of New York state manufacturing activity

Retail Sales numbers that measure a change in the total value of sales at the retail level.

Unemployment Claims which measure the number of individuals who filed for unemployment insurance for the first time during the past week.

Friday 6/16

Consumer Sentiment is a survey of about 500 consumers which asks respondents to rate the relative level of current and future economic conditions.

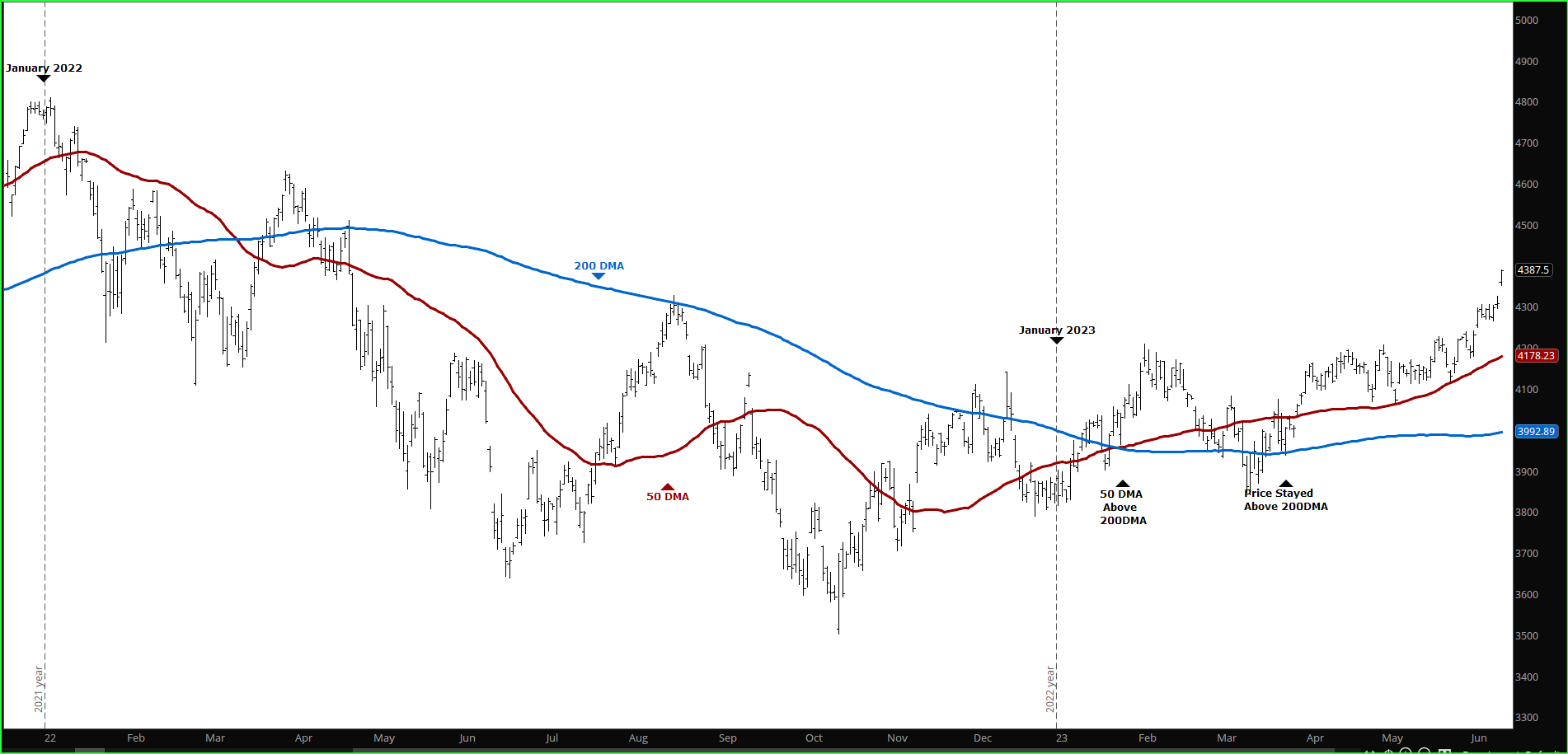

The chart below is of the S&P 500 Index beginning near the Markets top in January 2022 and continuing until today. The Red Line is the 50-day moving average and the blue line is the 200-day moving average. Markets that trade below the 200 DMA are considered bearish. As of March 23rd, of this year the S&P 500 has crossed above the 200 DMA and continues to stay above it, for the first time in over a year. In the beginning of April, the market crossed above the 50 DMA, which is considered a validation of its gaining strength.

While I do expect the market to show additional volatility during this weeks economic news announcements I am encouraged to see the recent strengthening trend.

The VIX Index: On Friday the VIX index closed at 13.83. On 5/1 the VIX was at 16.08. A falling VIX is generally bullish for the markets.

Percent of stocks above their 50-day and 200-day moving average: On 5/1, 59% of stocks were above their 50-day moving average, today 56% are above their 50-day moving average. Last month 54% of the stocks were above their 200-day moving average, today 54% are above their 200-day moving average. These numbers, while not stronger than last month are not showing any meaningful weakening in the markets.

Federal Reserve: The next Federal Reserve announcement will be on Wednesday June 14th. The CME FedWatch Tool at this time is predicting a 79% chance the Federal Reserve will not be raising interest rates. This Wednesday’s meeting will be very revealing.

Employment Rate: Total nonfarm payroll employment increased by 339,000 in May, and the unemployment rate rose by 0.3 percentage point to 3.7 percent, the U.S. Bureau of Labor Statistics reported Friday June 2nd. Job gains occurred in professional and business services, government, health care, construction, transportation and warehousing, and social assistance.

Inflation Rate: The annual inflation rate for the United States was 4.9% for the 12 months ended April, according to U.S. Labor Department data published on May 10, 2023. This follows a rise of 5.0% in the previous period. The next update on inflation is scheduled for release on June 13 at 8:30 a.m. ET. It will provide information on the rate of inflation for the 12 months ended May 2023.

The 10-year Treasury index yield: The rate today is at 3.76%. On May 1st it closed at 3.57%. The intra-day high so far for this year was on March 2nd at 4.09%.

To view past Market Newsletters, go to www.freedomcapitalmanagement.com. On the home page are recent newsletters, for older newsletters go to the blog page tab at the top of the home page.